I’m sure you saw the headlines about the bill passed last week. For Washingtonians, it caps off a few months of pretty substantial tax updates related to financial planning. Let’s go over it:

The Federal Tax Bill

There are a ton of summariesoutthere created by capable, professional pundits, but here are five of the most impactful changes I see affecting my client base as a whole:

Above all, the bill brings much-needed certainty in the tax planning world. Many of the tax changes put in place in 2017 were temporary and are being made permanent (‘permanent’ = ‘until they’re changed by a different Congress’). The most simple being tax brackets remain the same. This means we can plan things like Roth conversions, or how to tax-efficiently spend down retirement accounts, with more confidence. Moving forward, it’s still 10%, 12%, 22%, 24%, 32%, 35% and the final boss of tax brackets, 37%.

Somehow, the bill engulfs the most chaotic aspect of financial planning, student loans, into an even deeper level of chaos I didn’t think was possible. Forgiveness programs survive, but future borrowers — especially graduate students — will face lower federal loan caps and likely tougher private terms. Expect the real impact to unfold over the next few years.

The SALT (state and local tax) deduction expansion from $10,000 to $40,000 for joint filers may help Washingtonians who have big mortgages with big property tax bills. It also increases the paperwork burden for those who may need to track sales tax expenses to get additional deductions. For those who recently bought homes with high interest rates and have been disappointed to not get an opportunity to refinance yet, this one’s for you. (And be sure to book your appointment with your tax pro early)

The federal estate tax exemption moves up to $15 million for individual and $30 million jointly. There was real worry that this exemption was going to revert back to much lower levels, potentially forcing more Washingtonians to have to plan for future federal estate tax impact. For now, only households with very high net worth will need to continue engaging with their estate attorneys on the federal side. The state estate tax is another story — see below.

One piece of relief for working families with young children (of which I know there are many receiving this message), is the long-overdue expansion of the Dependent Care FSA contribution limit from $5,000 to $7,500. This doesn’t move the needle super far, but it’s progress and should put some money back in the pockets of those who utilize DCFSAs.

Tyler’s note: I’d be remiss if I didn’t mention that the bill has clear winners and losers. If you’re reading this then it’s likely you are part of the group disproportionately receiving the upside benefits. But you won’t have to look far or for very long, perhaps next door or within your own extended family, to see how the benefits were paid for. I keep it pretty politically neutral in these parts, but I don’t think it’s political to point out that our representatives spent their time “punching down” as they directed resources away from those who aren’t reading blog posts like this one. That doesn’t bode well for the long-term viability of the system we live in.

Personal commentary: Over.

Washington State Updates

We have an update to Washington’s estate tax. The exemption amount increases quite a bit to $3 million (nice!), but larger taxable estates see a much higher top rate at 35% (not so nice!). The takeaway is a constant refrain you’ve heard from me: This is a great time to update (or finally implement) your estate plan with an attorney if you’ve built up a significant net worth. Just let me know if you need help finding one or want to talk through the changes.

Similarly, the state has a new top bracket for long-term capital gains over $1 million (almost exclusively targeted at sales of stocks/bonds). There continues to be an exemption that changes every year (currently $270K), but the top rate now maxes out at 9.9%, up from 7%. This is another tax change that needs to be planned around, and will significantly affect those sitting on large gains from equity compensation or other concentrated positions.

As always, feel free to send me a response if you want to discuss any of the items above. Or schedule a 15-minute meeting. Or politely nudge someone you know to set up an intro chat.

The Wall Street Journal was out with a piece this morning, which describes a new product from mortgage lender Better.com that will allow Amazon employees to use their personal holdings of Amazon shares/RSUs as collateral for home purchases.

If you’re an Amazon employee, should you consider kicking the tires on this new product if you are looking to buy a home?

It’s pretty simple: I really don’t think you should do that.

Despite the stock being down. Despite this crazy housing market. Despite interest rates skyrocketing.

Let’s take a look at some of the reasons to not to use your Amazon stock or RSUs as collateral for a mortgage:

Enables (ongoing?) poor risk management. If you work at Amazon, you quite simply should minimize your exposure to the stock, not be looking for excuses to hang onto your shares. Working at Amazon and owning a significant amount of shares amplifies your risk (see: 2022/2023).

You will pay more than you otherwise would if you made a down payment with cash, like (almost) everyone else does. As stated in the article, the mortgage rate will be “between 0.25 and 2.5 percentage points above the market rate.” OK, so you’ll pay more to reinforce poor diversification.

It fails my #1 personal finance rule: It’s not simple. You should be relentlessly looking for ways to simplify your financial life, not make it more complicated. Perhaps you get a regular mortgage? *ducks*

It’s a mega behavioral bias exploiter. See the endowment effect (valuing something more just because you own it), the sunk cost fallacy (holding on to shares because selling could be admitting you were wrong) or confirmation bias (since this new product exists, it may confirm your [sorry to say] desire to hold too much stock).

Here’s why you should consider using your stock as collateral for a mortgage:

You’re very wealthy, your AMZN shares are mostly unvested, are a small percentage of your net worth, you’re looking to buy a multi-million-dollar home, you can’t manage to save money up for a traditional down payment and for some reason the rest of your assets are completely illiquid. If this describes you, by all means kick those Better.com tires!

If allowed to speculate, and I will (because this is my microphone), I’d say the marketing team at Better.com has this line of thinking:

“This housing market is terrible! We need to sell more mortgages.”

“Let’s think of niche strategies to target certain groups of individuals. I know, Amazon.com is the 2nd largest private employer in the country!”

“Hold on, it looks like they’re paid with a lot of stock, and the stock has been crushed. How can we leverage the fact that they might be trying to hold on to get back to even?”

“A custom, collateralizaed mortgage product!”

Alright, that’s the end of the heavy sarcasm. But I’m willing to bet that more or less this is what happened over at Better.com.

It’s a bit concerning that Amazon has signed off on the program to some degree by releasing a statement about it, and even going far as stating that it “aligns with Amazon’s benefits program that seeks to care for the financial wellness, mental wellness and physical wellness of its employees.”

I’d argue that playing off of several behavioral biases as a strategy to convince employees to further hold on to company equity is not exactly promoting “wellness,” but to each their own.

I’M NOT MAD AT ALL ABOUT THE RIDICULOUSNESS OF THIS WHOLE DEBACLE, OLYMPIA, IT’S JUST A SOFTWARE QUIRK THAT HAS TURNED THIS INTO ALL CAPS AND INCLUDED THE FOLLOWING EXCESSIVE EXCLAMATION MARKS!!!

Now that we’ve all hit a pillow, what are Washingtonians supposed to do now, given that the Powers That Be have put WA Cares Fund on hold? Here are my thoughts:

If I were to handicap this outcome, I’d say there’s about a 50% chance the Cares Fund is doomed, either by being delayed into oblivion by the state Legislature or it’s made optional by Initiative 1436.

The remaining 50% chance would be of some kind of significant reform to the program, which has many qualities in need of significant reform. I also suspect this would bring opportunity for those locked out of the opt-out process, for one reason or another, to get another shot at bowing out.

If you purchased a long-term care insurance policy solely for the opt-out

I’d hold tight. Do not declare victory just yet. You certainly don’t want to cancel your private LTC policy, only to see the rules of the game change in 2022 and now you could be stuck in the program for life. It’ll be best to watch the headlines and see how this unfolds.

If you decided not to purchase a policy for the opt-out

This is your chance to reconsider that stance, especially if the rules are going to be modified. From my experience helping clients this year, there’s a certain level of “I just don’t want to deal with this,” but it very well may pay handsomely to Deal With This. Same conclusion: Let’s see how this pans out, and you can evaluate again.

If you weren’t able to opt-out, but wanted to

Happy Holidays! This is appears to be a huge gift coming your way. I can’t imagine a scenario where the program survives but they don’t allow for a new opt-out period, or some kind of other help. I have to think this gives you another shot at applying for a private long-term care policy to qualify yourself exemption from the tax. Again, let’s see how the news unfolds and then you can act accordingly. It won’t hurt to reach out to insurance carriers now so you have an established point of contact moving forward.

One big risk for all groups:

There’s a chance the favorable loopholes get closed. By all indications this program was going to be a one-and-done opt-out – you get your private policy, apply for exemption, then you’re out of the Cares Fund tax for life. But I don’t know if that will survive this reset, because it’s a huge loophole for wealthy individuals or those who have financial planners on the team. This means Washingtonians may have to keep their private LTC policies in place to continue with the opt-out, and possibly prove it’s in place yearly moving forward.

No matter your situation, the overarching conclusion is the same: Stay tuned, evaluate the developments according to the impact on your own personal finances, and act quickly when the news drops.

Say what you want about Andrew Yang and the ‘Yang Gang,’ but the MATH slogan is excellent. Source: yang2020.com

Most Washingtonians know what BECU is. Formerly a credit union with a closed field of membership for Boeing employees only, BECU, now open to the public, is Washington state’s largest credit union at over $20 billion, has more than a million members, and is the 4th-largest credit union nationally. They’re about seven times bigger than the nearest in-state credit union competitor. Coincidentally, they’re headquartered in the same city as this blog, so you can consider this a domestic dispute between neighbors. But enough background, let’s talk about BECU interest rates on deposit accounts.

So, what’s the beef? It’s all about the way the advertise their interest rates. Take a look:

Innocent enough, right?

Wrong.

Seeing that 6.17% interest rate flash on the screen is a show-stopper. The record player screeches to a halt and a burning question flashes on the mind of anyone with a decent handle of current interest rates (or math):

“What the hell?”

This rate is triple anything else considered competitive in the marketplace, which raises all kinds of red flags and trips any bullshit detector that’s even remotely calibrated.

Yeah, that completely deceptive 6.17% APY. And the second line disclosure doesn’t get them out of the penalty box.

So many things come to mind, but first, here’s the ultimate conclusion: BECU should stop doing this kind of deceptive marketing. It’s Wells Fargo slimy. It’s payday lender garbage. And it’s nice to be innovative, but using teaser rates for deposits is not exactly the kind of innovation I’d recommend.

So what exactly is it that ties together Wells Fargo, payday lenders, and this marketing from BECU? Preying on people who just don’t know any better. People who just aren’t very good at math. Or people who know a little, but not enough to know better. They might know that BECU has a good rep, and that they should be looking for high interest rates – which could be plenty of reason for them to open an account. Unfortunately, we see this kind of deception, fine print and obfuscation everywhere in the world of financial shenanigans.

The banking industry is hyper competitive, where most products and account features are now table stakes, so people are often left comparing institutions based on interest rates, especially now that rates have normalized after the financial crisis. And let’s be real – people don’t dig much further than what’s on the surface (or in the largest font). Therefore, you’d imagine a lot of people are seeing this 6.17% rate and concluding it’s a great deal. And, let’s be honest, most people aren’t very good at math. Do you think BECU doesn’t know this?

The $30.85 Math Deficiency Dividend

The truth of the fine print is that the BECU interest rate policy is effectively wagering $30.85 (the $500 maximum multiplied by the 6.17% teaser rate) in “additional” interest payment to acquire prospective customers who probably don’t know that their rate is deceptive, or that it reverts back to effectively nothing (0.10% APY) after $500 in deposits.

If you plop down $10,000 into a BECU savings account – a pretty small emergency fund – the net rate you receive is 0.40% APY, or $40.35 in total annual interest. That’s (6.17% x $500) + (0.10% on the next $9,500) divided by $10,000. Plenty of other institutions are offering BS-free rates four to five times higher than 0.40% APY. If you’re evaluating BECU as a destination for an emergency fund, I encourage you to look elsewhere. Unfortunately, BECU probably wants consumers to conclude “BECU has good rates” with this kind of marketing.

Can you guess which kind of customers are really good for banks? People who aren’t likely to be financially literate. They pay more fees than otherwise more educated people.

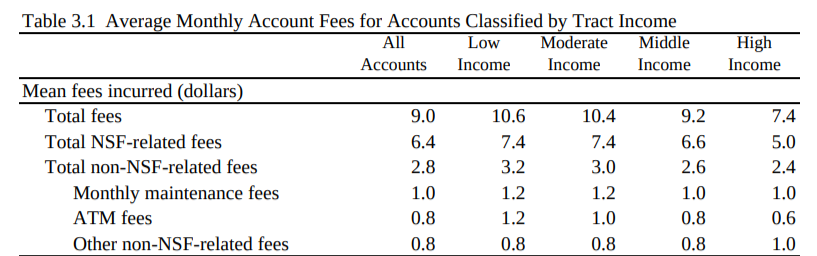

A 2014 study of large banks produced by members of the FDIC, CFPB and the University of Michigan showed, among many interesting data points, two very relevant tidbits:

High income account holders were much more likely to have college degrees (47.4%) than low income account holders (17.7%)

Most importantly: Low income account holders paid 43% more in monthly fees ($10.60) as compared to high income account owners ($7.40).

The poor pay more.

I think you can see what I’m getting at: It’s more profitable to have low income account holders, who are more likely to be less educated.

And just how might one go about getting those less educated account holders? Why, how about some misleading marketing!

Now, if I’m BECU, I might respond by saying that *insert stern tone* “On a risk-adjusted basis, accounting for lending income and charge-offs, your assertion that we are preying on low income customers is just preposterous!”

OK, cool. But it still doesn’t explain why this kind of marketing needs to be employed, especially when BECU is all up on their high horse about not being another one of the big banks where slimy marketing/schemes are routinely employed.

Why not just a new account bonus?

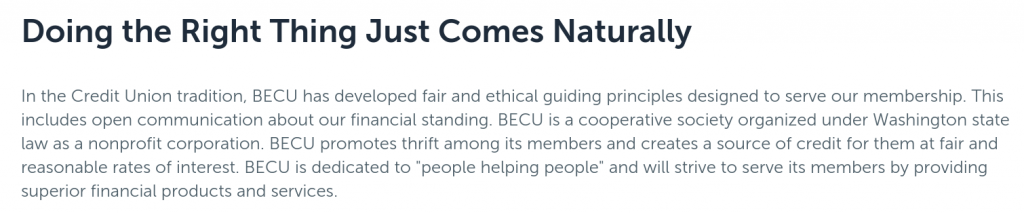

This passage from BECU’s Governance page is a bit cringeworthy if you start thinking about what’s right and wrong in banking.

Plenty of banks simply offer a sign-up bonus. We’ve all seen these offers somewhere. And BECU is not reinventing the wheel by incentivizing people to open new accounts.

Sign-up offers are nothing new.

It’s the way BECU is going about offering this $30.85 bonus. Personally, I think it’s sinister and has to be downright embarrassing for those in the organization who want to truly do right by their membership. If viewed as a sign-up bonus, it’s weak compared to competitors. If they offered savings rates at, say, a more honest 0.40% APY, it’s also weak compared to competitors.

Some parting questions:

Where is leadership? BECU’s well-compensated board members seem like they have pretty busy day jobs, but I still don’t know how they’re giving this a pass.

Has BECU officially become too big to remember what a credit union is supposed to stand for?

If BECU members were polled, what percentage of the membership would state they are customers in part to the high interest rates they *think* they’re receiving on checking and savings?

Why 6.17%? I think I know, but I’d love to hear an answer. Something tells me it’s completely random and irrelevant because it’s there to draw attention. Maybe they had the meeting on June 17th.

Does BECU deserve your money?

With all of this said, this doesn’t necessarily mean BECU should be thrown out as a prospective banking institution. Even I, executioner of bad financial products, am not giving them the full no-go. I know I’m harping on a pretty niche subject. It does, however, fully cement the thought that they are absolutely no different than the big banks now. No longer should anyone consider BECU as some kind of crusader for good in the shady world of personal banking. And don’t buy the sales pitch they they’re a beacon of moral authority or one of the “good guys.”

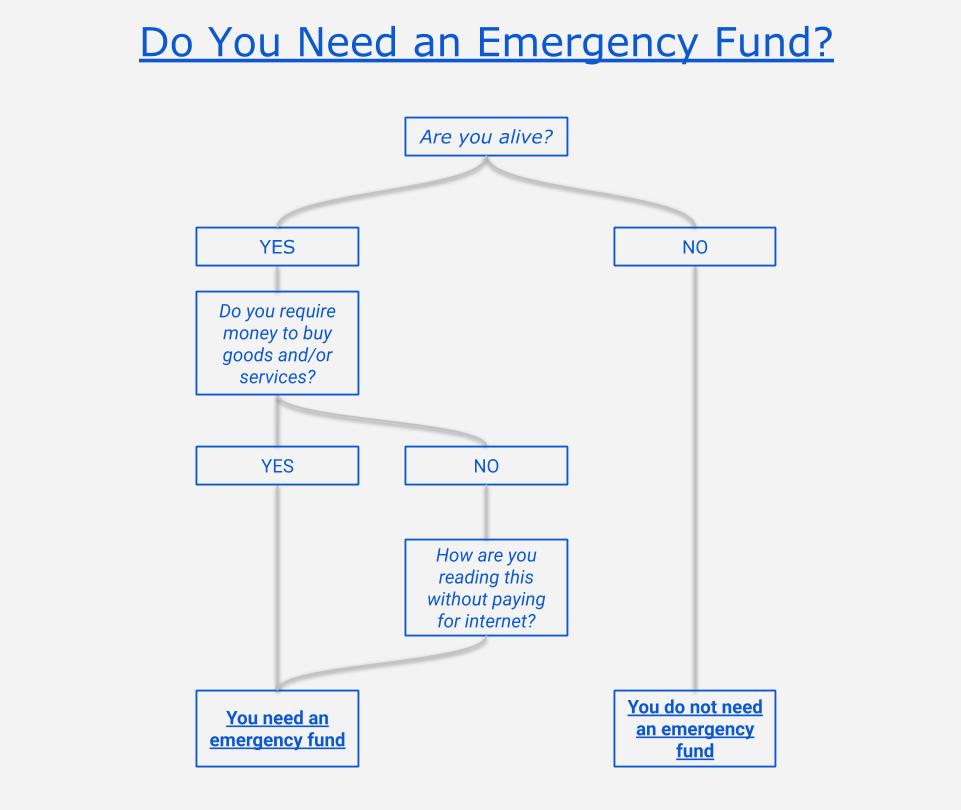

There is nothing more fundamental to a healthy financial life than a fully stocked emergency fund. And there are many guides to emergency funds, but this one is mine.

I made this flow chart for you, dear reader.

Do you really need an emergency fund?

Some people like to think they’re immune from needing an emergency fund, giving reasons like “I’m retired” or “I have too much debt” or “I’m ridiculously wealthy” or “I have a very stable job and no debt” or “I live in self-sustaining bunker.”

But let’s get down to the definition of what an emergency fund actually is:

An emergency fund is simply a stash of money you only touch in cases of, well, emergency. (More on the definition of “emergency” later)

This means all of the above excuses are rendered moot.

Retired people need a stable, liquid pool of money in case any number of things happen – like large healthcare expenses – and especially as a buffer from feeling emotional about short-term market swings.

People deep in debt need an emergency fund because it’s simply the first step in the process of emerging from a negative net worth to a positive net worth. (True, it’s the same as saying, somewhat obviously, that they need to be out of debt)

“Ridiculously wealthy” people need an emergency fund because it’s a vulnerability to have all assets tied up in investments or illiquid property.

People with stable jobs and no debt need an emergency fund because a stable job is only as good as the economy, industry, or government their occupation serves.

The bunker people are already proving my point because their whole shelter is an emergency fund full of, presumably, dry goods and ammunition.

An emergency fund primarily functions as an immunization from all of the possibilities that everyday life brings all of us at one time or another. This would be the “lovey blanket” factor, as I like to call it. An emergency fund is a comfort in the face of uncertainty.

Most importantly, you need to be able to survive today to be able to plan for tomorrow. An emergency fund is key to that survival.

So, we’ve settled it. Everyone needs an emergency fund.

How much money do you need to keep in an emergency fund?

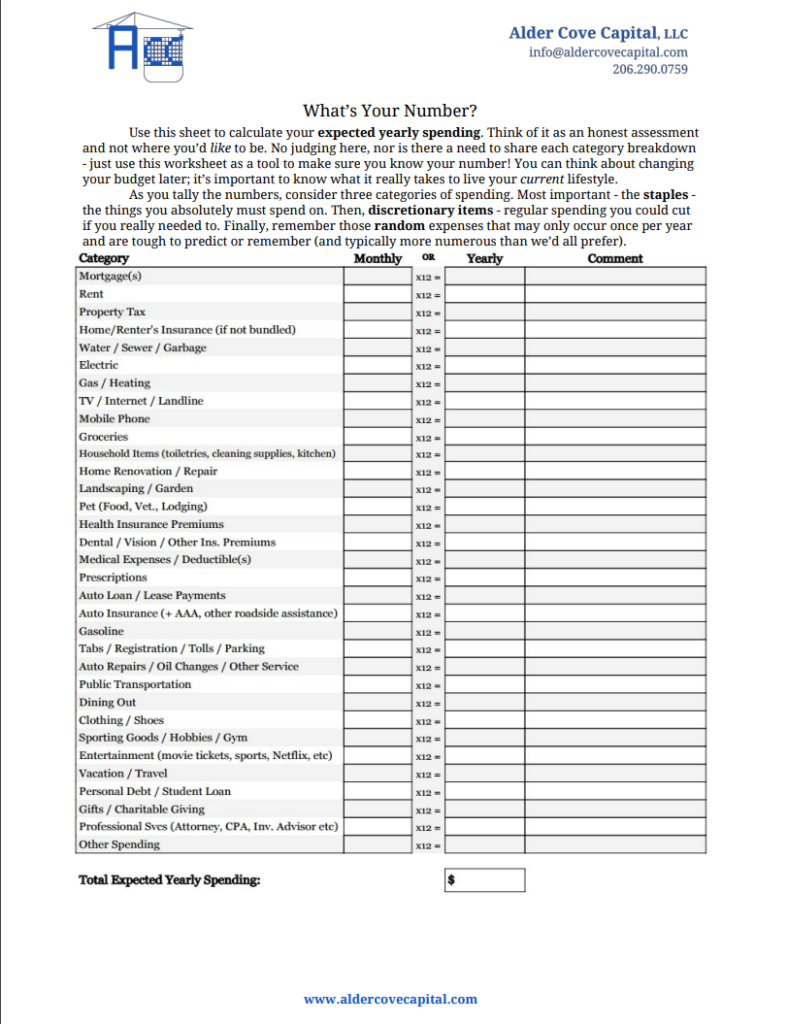

There are many different rules of thumb, but I generally recommend keeping three to six months’ worth of expected annual spending as an emergency fund, which translates to 25% to 50% of what you expect to spend annually on an ongoing basis.

This means you’ll need to know how much you expect to spend. You can figure out this number by using my one-pager here, or create your own copy in a digital version here. And don’t turn it into a budget – just an honest assessment.

Three to six months is a guideline, but given that the average length of unemployment is currently about five months, I definitely don’t recommend going less than three months because that puts a heck of a lot of pressure on someone to get a new job in the event of a disruption of employment or a very large unexpected expense.

Factors encouraging a larger emergency fund, all else equal:

High debt levels relative to income

Having dependents

Known health issues

Working in an economically-sensitive industry (businesses more likely to rise and fall in cycles)

Unpredictable patterns of income, and/or when self-employed or working for a smaller company

Factors encouraging a smaller emergency fund, all else equal:

Low debt relative to income

No dependents, or having a two-income household

Good health

Working in a stable industry (think healthcare, education, government)

Salaried income or pension/annuity income

Having a high savings rate

Having a high risk tolerance

Sufficient disability/auto/home insurance

Low deductible health insurance

Diversified investment portfolio

Where should your emergency fund live?

Simple: A high-yield savings account, most likely in an online-only format to get the best rates. Here’s an example of the difference between the average rates offered by online and in-person branches over the last five years:

After a years-long marathon of interest-free deposit accounts, we’ve finally made it back to the world of getting a decent rate of return on savings products. It might not last long, but right now you can get a 2% annual yield with many reputable institutions.

Paying a decent interest rate is important because this will allow the account to at least have a chance at keeping up with inflation. Plus, free money is nice. A $50K emergency fund will produce $1,000 in interest per year right now. That’s not nothing.

Just make sure the account is FDIC-insured (or NCUSIF at a credit union). Also confirm your account doesn’t exceed deposit insurance limits (generally $250K) – but most people won’t have to worry about this for an emergency fund.

To compare accounts, Bankrate and NerdWallet have pretty good screeners.

What constitutes an emergency, anyway?

Suze says no.

This is the really subjective part. You could say I’m an emergency fund fundamentalist, because I don’t believe in using the account as a slush fund. There are only a few reasons you should ever take money from this account:

Job loss

Paying for a high medical insurance deductible or coinsurance

Any incidents/accidents that can’t be reasonably (or aren’t) covered by insurance*

That’s it.

No, not that other thing you just thought of. Only job loss, medical deductible/coinsurance, and only the craziest random things.

This is not a stash to be raided for vacation, (especially not) for buying a home, for home renovations, for buying a car, for fixing a car, for getting a new roof, for yada, yada, and/or yada.

Let’s talk about that “*” above. The phrase “can’t be reasonably covered by insurance” is an important one. Most of these instances will end up with the final verdict of “you should have allocated for that in your expected spending” via insurance premiums or deductibles. This means, for instance, that having to spend a chunk of money for auto insurance deductibles or auto maintenance should be planned for. Or your insurance policies should be structured so that a paying a deductible doesn’t necessitate emergency-like spending.

Why not a new roof? Simple: Replacing a roof shouldn’t sneak up on you. It’s an expense that should be planned and saved for over the span of years. Now, a random roof leak would be different. It certainly would be unexpected and should be considered an emergency because it’s unlikely that homeowner’s insurance will cover it if it’s normal wear and tear or negligence (it also needs to be urgently fixed).

A lot of this comes down to your expected annual spending. If a spending item falls into any of the categories listed on the sheet I provided, it probably will be denied from being bailed out by your emergency fund. Own a home? You better be putting a huge number down for “Home Renovation / Repair”. Same in the auto category: If you own a car and leave “Auto Repairs / Oil Changes / Other Service” blank, then you, my friend, have built a BS Budget.

Biggest of all, your “Other Spending” category sure as hell better not be blank. That’s where you allocate for all the random spending that would be impossible to predict – and it’s not unreasonable to have it equal 10% of your expected annual spending.

Your emergency fund has two best friends

Insurance is the key to stabilizing the firewall around your emergency fund, but it’s also aided by keeping a healthy “float” in your checking account.

First, insurance allows you to hedge against most of the low-probability / high-cost events you could face (death, disability, flood, fire, earthquake, theft, burglary, severe illness, car accidents, even lawsuits or professional liability – the list is long).

Second, a healthy float in your checking account will allow you to pay for some the random non-emergency items that arise. This lowers the tendency to run to the emergency fund for a quick buck. Simply take your expected annual spending and divide by 12. You should seek to have a month’s worth of spending remaining in your checking account at all times. For a household expecting to spend $90K per year, this buffer should be set to roughly $7,500. After all the normal bills are paid, this buffer will finance things like the random new bumper, new oven, or tickets to the Hawaii trip. If your checking balance goes below one month or above two months of spending, then it’s time to re-calibrate.

How do you build an emergency fund from scratch?

Yes, it’s daunting. If you don’t have the funds to just throw a huge chunk of change over to a high-yield savings account, you might see this as an impossible task.

Two steps will aid in fully funding your emergency fund:

1) Treat it as an expense: Choose a date you think you can reasonably get the account fully funded. If that day is three years from now, then a monthly expense for your emergency fund is the equivalent of 1/36th of the fully funded value. (A $30K fund would need roughly $833 in monthly deposits to reach its goal in 36 months)

2) Automate: This part will create a forced commitment to the step above. You’re more likely to keep to the goal of forced saving if it’s something you have to turn off to disrupt. Get the courage to set up an auto-deposit and commit to treating it as a fundamental necessity to your annual spending. Nothing will get you to truly consider other spending than automating this step.

We’ve covered why you need an emergency fund, how much to keep there, where it should live, when it’s OK to spend from it, and how to begin building one. Anything you think I missed? Questions about emergency funds? Let me know your thoughts.